In recent years, information about new financial and accounting centers or shared services centers (SSC) for globally operating companies has appeared more and more frequently. Specialized organizations providing business process outsourcing (BPO) are also being established.

Due to many social and business factors (lower labour costs, access to highly qualified personnel, cultural affinity and low level of business risk, among other things), Poland is perceived as a very attractive place to locate shared services centers for international corporate groups here or also to avail of BPO services. In our country, the largest groups’ new shared services centers have been gradually being established for several years now. Some of them provide services for the entire group, while other support .e.g. a region of Central Europe.

This global trend is clearly noticeable among Polish companies as well. The multi-branch organizations and corporate groups operating locally also see the benefits of combining such functions as e.g. accounting functions within the company carved out for this purpose.

What kind of shared services

The establishment of a shared services center consists in carving out, transferring and consolidating the selected services to the carved out, specialized unit that will handle both external and internal customers while maintaining the specified level of service provision – SLA (service level agreement). The basic difference between a shared services center and an accounting services center lies primarily in the activity range.

By definition, an accounting services center provides services connected with keeping records of accounting documents and accounting and settlement methods. Additionally, it is responsible for preparing financial documents and statements that are required by law both within the organization and beyond it.

The shared services center, in addition to the above-mentioned accounting processes, is also responsible for executing additional functions provided for the benefit of other companies or entities within one organization, e.g. in the area of payroll, central execution of purchasing processes of e.g. key raw materials, management of master data change and creation (e.g. materials and vendors), preparation of reports (both required by law and for the internal corporate needs).

The shared services center usually performs significantly more functions than the accounting services center and does not focus its services solely on accounting, but comprises also other areas of the company’s activity.

Centers for IT infrastructure management in a corporation represent a separate category. In particular, they operate in those companies that have corporate systems for integrated management, requiring continuous administration and development. They may be a part of a company’s shared services center or they may operate as a separate entity.

Shared services center – for whom?

While considering the creation of a shared services center that supports the processes within the company, you should first consider what services should be rendered centrally and next, what benefits can be achieved through the establishment of such a center. In a traditional model of a company operation, particularly of a multi-plant and geographically scattered company, the following attributes are distinguishing:

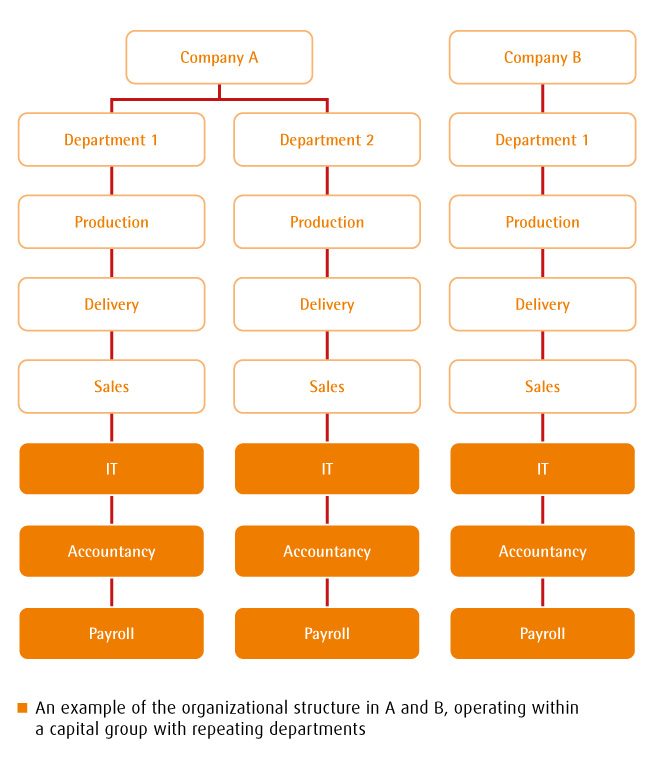

- copying of the organizational structures in particular companies of the group,

- high probability of lacking uniform procedures and standards in the group companies in the accounting area, e.g. lack of common chart of accounts,

- possible lack of uniform rules for settlements with vendors and customers, e.g. inconsistent discount policy, various payment terms,

- necessity of making additional settlements between particular companies within the group,

- no possibility of using the economies of scale, e.g. not making use of a better negotiating position provided by joint purchasing,

- potential low effectiveness; lack of indicators to measure and verify the effectiveness of the organization; inability to compare the efficiency of particular companies,

- copying of the same posts in the particular branches’ organizational structures.

As opposed to the traditional model, concentrating the processes and their execution in the shared services center may help to achieve many benefits through:

- high effectiveness resulting from high specialization,

- uniform procedures and standards of cooperation within the group and beyond it (for contacts with banks, vendors and customers),

- transparency of the processes – clean-up of accounting and other procedures along with easy verification of business transactions,

- reduction of process maintenance and operating costs,

- creation of one contact point for customers and vendors,

- possibility of specifying and parameterization of coherent indicators for the assessment of the organization’s effectiveness.

The advantages that are presented above may be achieved irrespective of whether the shared services center of the organization will be a dedicated, formally separated company or a department that is organizationally carved out, or whether the company will use the services of an external organization, e.g. services pertaining to payroll.

Which processes should be centralized

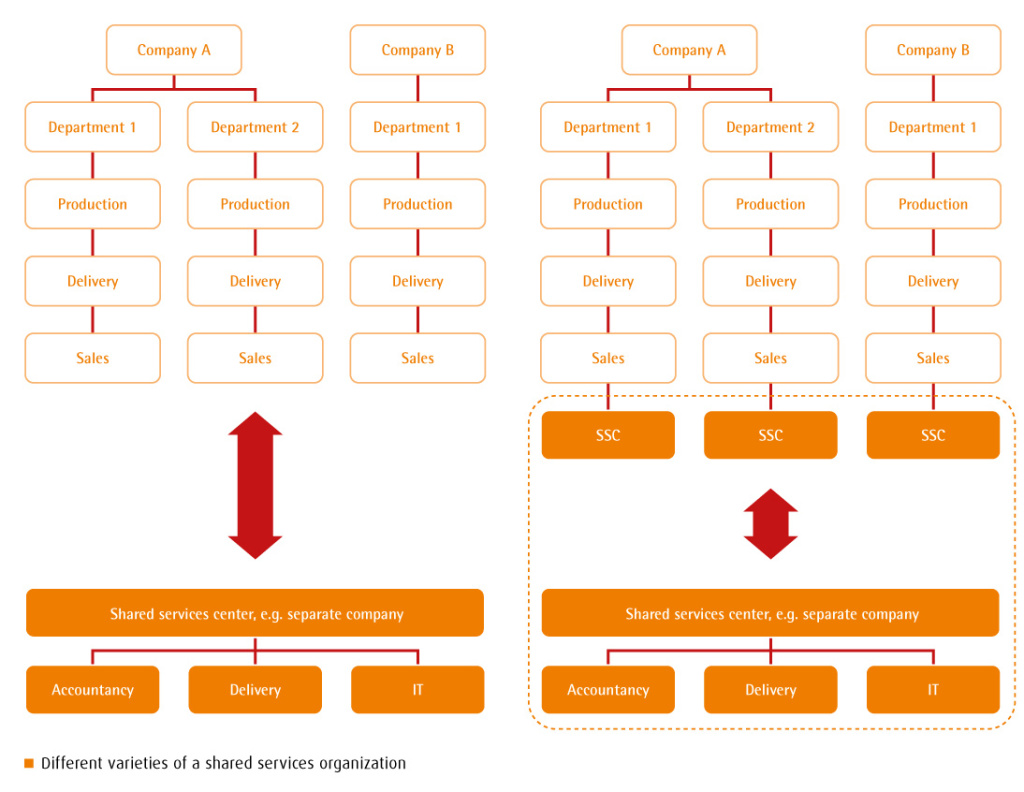

Creating SSC does not always mean centralization. The practice shows that not all business processes in a company may be centralized and the centralization does not always guarantee achieving the synergy effect. A classic example may be the centralization of purchasing processes. It is certainly reasonable with reference to purchasing raw materials or packaging, but if you purchase e.g. spare parts for machinery and equipment, it is recommended to make purchases through the local purchasing departments.

It does not mean that the local department cannot be a part of SSC. The diagram below represents examples of two varieties of a shared services organization. In the second variety, it was assumed that part of the processes will be executed locally, in particular plants. Such organization of a shared services center – with local units of SSC is justified in organizations where particular companies differ significantly from one another with reference to their business activity profile (e.g. different production profile, sales channels, separate production and distribution companies etc.).

The project of creating a shared services center in an organization usually comprises four basic areas of activity:

- creation of business concept and development of target processes,

- implementation and adaptation of IT tools,

- execution of organizational changes and preparation of qualified resources,

- selection of location.

Business blueprint

The business blueprint of SSC should include the detailed scope and description of services provided. When you create assumptions for making particular steps in processes, it is necessary to consider many factors, e.g. what influence the changed processes have on other areas of business activity. Potential changes in areas related to the SSC activity should remain part of the work on the concept of the center’s operation. Creating a matrix of SSC’s responsibility, defining the scope of responsibility and authorizations for particular posts, and additional factors (e.g. SOX) is all good practice.

The concept of SSC should also specify how to measure the effectiveness of particular processes and which IT tools should support the work in the newly created center.

IT tools

While implementing the IT tools or adapting the existing ones to the requirements of SSC, it is worth remembering that such projects are primarily business projects, and IT projects only secondarily . Nevertheless, the integral part of the business blueprint should be the part referring to changes in the IT. For example, if we ultimately use the electronic document flow, special attention has to be paid to the development of particular steps in the process and implementable functions in each step. Such a description should be accurate and detailed.

The analysis of the IT technical infrastructure is another issue. Integrating the hitherto geographically scattered tasks in one place of may also require purchasing IT equipment and creating or modifying used tools for e.g. scanning invoices. Such activities should be planned and provided for in the project schedule and budget.

Organizational changes, personnel, selection of location

The creation of SSC entails great organizational changes in companies. Considering the new organizational structure and rules for managing the center, along with the employment strategy (transferring and rearranging employees, recruitment of new ones etc.) is one of the elements in the concept works on SSC.

The introduction of changes connected with the change of processes in each organization, and particularly in the territorially dispersed organizations, requires adopting change management. Starting SSC will be noticeable not only within the company, but also for its business environment (vendors, contracting parties), and therefore the information policy and change management should be concentrated not only on the organization, but also on the external environment.

Selecting a location for a shared services center depends, to a large extent, on economic factors (lower labour costs, low rental cost), availability of qualified staff (proximity to academic centers is a favourable factor) and available infrastructure.

SAP system for the shared services center

The organizational changes are connected not only with new procedures, e.g. with the determination of new paths for document approvals, but also with the necessity to create and use new work tools – IT solutions that are to support business processes and facilitate their partial automation, for example in document flow and document approval.

While working on the concept of the shared services center, the stage of developing and implementing the new IT system or, if such system exists in the company, the stage of its adaptation, is an integral part of the project.

At BCC (now All for One Poland) we know from experience on projects related to implementation of processes supporting the shared services center’s handling in SAP ERP system changes, the necessary adaptations refer in many cases to the following areas:

- changes in the purchasing processes connected with the centralization, for example entering contracts, framework agreements,

- using the EDI mechanisms for posting of purchase and sales invoices as well as customer purchase orders,

- using data warehouse for creating new reports that facilitate reporting and analysis of the entered data,

- workflow for the approval of purchase invoices,

- workflow for the master data management,

- workflow for the approval of requests, purchase requisitions and purchase orders,

- devices for scanning and labelling the incoming invoices.

What to consider

Carrying out the SSC carve-out project, like any project, is connected with some recurring challenges. Performing a risk analysis, it is worth paying attention to the following aspects:

- lack of availability of qualified staff,

- potential problems with processing multi-language documents,

- necessity to introduce the IT tools allowing for the processes to work using workflow and for processing digital documents – often these solutions are not provided by one vendor.

- in the case of an international organization, it is necessary to consider the local specific character, e.g. in relation to accounting or payroll,

- insofar as possible, the introduced solutions should be uniform – the solutions specific for different plants should be restricted if possible,

- introduction of changes requires time and adaptation of the organization.

The establishment of shared services centers or accounting centers has already been a proven business practice. This trend results above all from economic benefits that an organization may enjoy. It is not without significance that there are also other factors – the effectiveness and quality of work is increased. The time of performing particular activities is shorter, maintaining an adequate level of services. In a centralized organization, a higher qualification of employees and thus better parameters of services quality may be strived for.

Essential organization units are released from repetitive actions that are not related to their primary business activity. The shared services center allows using the economies of scale and minimizing the costs, e.g. of the required IT tools, the maintenance of premises and staff.